A LOW INTEREST RATE IS GREAT BUT IS IT THE ONLY THING?

Posted on 09/11/2018

Debt Reduction – It’s more than just having a cheap interest rate.

When assessing home loan options, people are always drawn to accessing the lowest Interest rate. YES, I agree this is very important however, there is much more to consider if your financial goal is to pay out your home loan sooner.

With so many options available in the market place it is important to ensure you have a product that is both tailored and offers the flexibility that you require. The ultimate goal is to make this work for you and your current situation. As a debt specialist, it is my responsibility to custom design a home loan structure that meets your needs and makes life easier.

Effectively using an Offset Account is a great tool to help you be debt free sooner. Moreover, accessing multiple offset accounts linked to the same loan has the ability to empower your debt reduction strategy and make cash flow management a little easier.

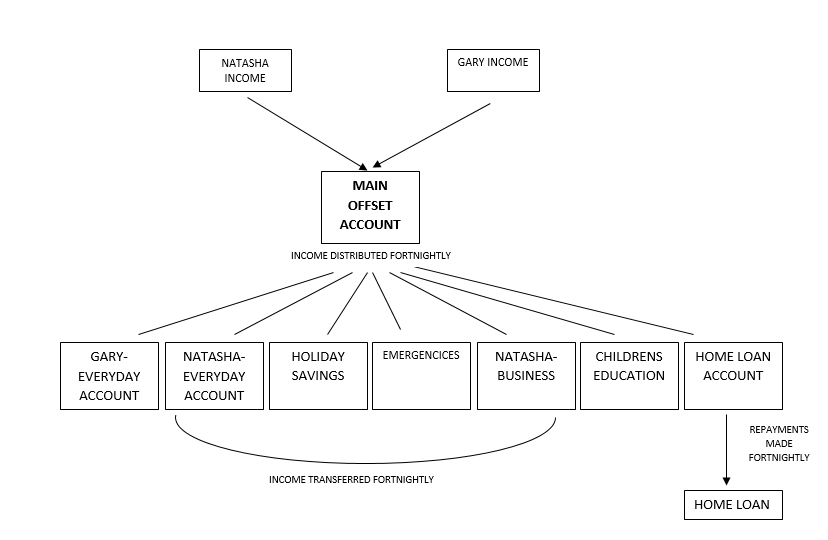

An offset account is a transaction account linked to your home loan. Its balance is ‘offset’ daily against your home loan balance; resulting in only being charged interest on the difference between the two. Many lenders are now offering up to 10 separate offset accounts linked to one home loan account. Below is an example of a recent client scenario which we have implemented that will progress our clients to a debt free position sooner.

Gary and Natasha are a married couple with 3 children. Gary is employed at VISY and Natasha runs her own osteopath business. They have a home loan which they are trying to pay off as well as two credit cards which are meant for emergencies but have recently been used due to an overseas family holiday.

Gary and Natasha under their new structure use MULTIPLE OFFSET accounts to budget for the family holiday, emergencies and keep Natasha’s business funds in a separate account. Their banking structure looks something like this:

In addition to employing multiple offset accounts we also changed their LOAN REPAYMENT FREQUENCY. As both clients are paid fortnightly, we updated their repayments to be in line with this. The benefit of making an extra repayment per year over a 30-year loan term will reduce their loan term and the interest payable. As illustrated from the table below this change alone is a significant saving.

In addition to employing multiple offset accounts we also changed their LOAN REPAYMENT FREQUENCY. As both clients are paid fortnightly, we updated their repayments to be in line with this. The benefit of making an extra repayment per year over a 30-year loan term will reduce their loan term and the interest payable. As illustrated from the table below this change alone is a significant saving.

|

|

Monthly

|

Fortnightly

|

Repayment Amount

|

$2,387.08

|

$1,193.54

|

Loan Term

|

30 Years

|

25 Years, 11 Months

|

Interest paid over loan term

|

$859,347.53

|

$802,964.08

|

Gary and Natasha will save 4 years and 1 month of their loan and over $56,000 in interest. This does not even take into consideration any offset account benefits.

If you too wish to TAKE CONTROL of your debt like Natasha and Gary, then take advantage of our debt reduction strategies by contacting our office for a complementary assessment of your position.

The case study is illustrative only and is not an estimate of the investment returns you will receive or fees and costs you will incur.

This document contains information that is general in nature. It does not take into account the objectives, financial situation or needs of any particular person. You need to consider your financial situation and needs before making any decisions based on this information.

If you decide to purchase or vary a financial product, your financial adviser, AMP Financial Planning and other companies within the AMP Group may receive fees and other benefits. The fees will be a dollar amount and/or a percentage of either the premium you pay or the value of your investment. Please contact us if you want more information.

ASCK Pty Ltd atf the AMEGAFS unit trust (ACN 105 450 566) trading as AMEGA Financial Solutions is an Authorised Representative and Credit Representative of AMP Financial Planning Pty Limited ABN 89 051 208 327 Australian Financial Services Licence 232706 and Australian Credit Licence 232706